Desirous about shopping for an annuity? At first look, it’d look like a great retirement funding. However wait! Don’t signal that dotted line simply but. There are some things you want to know about annuities earlier than you commit.

What Is an Annuity?

An annuity is mainly a contract between you and an insurance coverage firm. It’s designed to supply a assured revenue for the remainder of your life. You make a fee (or funds) to the insurance coverage firm. In return, they promise to develop your cash and ship you funds throughout retirement. Annuities are sometimes marketed as monetary merchandise (like shares, bonds, and so forth.).

The last word aim of an annuity is to offer you a gentle stream of revenue all through your retirement, which sounds nice at first. However are annuities actually one of the simplest ways to safe a stress-free retirement?

Let’s take a more in-depth have a look at what annuities are, how they work, and whether or not they need to be a part of your retirement financial savings technique. Spoiler alert! Typically—the reply to that final query isn’t any.

However regardless of that, annuities are extra standard than ever. Why? Properly, with uncertainty swirling across the economic system, Social (In)Safety and pension plans drying up, many individuals are in search of steady revenue streams for his or her retirement.

Solely 29% of Individuals say they’re very assured they’ll come up with the money for to reside comfortably all through their retirement years.1 That may clarify why greater than half of employees could be very inquisitive about an annuity if it was supplied by way of their employer’s retirement plan.2

Insurance coverage firms promote numerous annuities by taking part in on individuals’s worry of outliving their retirement financial savings. However once you boil it down, annuities are an insurance coverage product. You’re paying an insurance coverage firm to tackle the danger of you working out of cash.

That’s the easy model of what an annuity does. In actuality, annuities are tremendous sophisticated and are available in a number of completely different styles and sizes. It’s sufficient to make your head spin. However persist with us. We’ll break it down for you.

How Do Annuities Work?

Placing an annuity collectively is quite a bit like ordering a burrito at Chipotle, simply not as tasty. The annuitant (you) can create an annuity primarily based in your preferences and your personal private scenario, minus the chips and guac. Listed below are the alternative ways you may put an annuity collectively.

Single vs. a number of premiums: How do you wish to pay for the annuity?

You probably have a giant pile of cash—perhaps by way of years of saving or an inheritance—you may pay for an annuity in a single massive fee. Or you may pay for the annuity with a sequence of funds over a few years. This era once you’re contributing cash is known as the accumulation section. And the cash you set in grows tax-deferred—which suggests you solely pay taxes on that cash once you begin getting your funds in retirement.

Instant vs. deferred: When do you wish to begin getting funds?

You possibly can select whether or not your annuity pays you straight away (rapid annuity) or in some unspecified time in the future sooner or later (deferred annuity). Take into accout, if you happen to take any cash out of your deferred annuity earlier than age 59 1/2, you’ll get hit with a ten% early withdrawal penalty on high of the revenue taxes you’ll owe!3 And we haven’t even touched on annuity charges but. Simply you wait.

Lifetime vs. mounted interval: How lengthy will you retain getting annuity funds?

Along with selecting when you’ll begin receiving annuity funds, you’ll additionally must resolve how lengthy these funds will final. One in every of your choices is a lifetime annuity that pays you a specific amount monthly for the remainder of your life. Or you could possibly go together with a set interval annuity that’ll ship you funds for a set period of time—wherever from 5 to 25 years.

Varieties of Annuities

Now that we’ve laid out how annuities are arrange, let’s have a look at the completely different varieties. There are two most important forms of annuities—mounted and variable.

Mounted Annuities

Mounted annuities are mainly financial savings accounts with an insurance coverage firm. They’re like a certificates of deposit (CD) you will get at most banks. They arrive with assured rates of interest (at the moment lower than 5%), and that’s tremendous engaging for individuals who need a predictable and “secure” place for his or her cash.4

![]()

Market chaos, inflation, your future—work with a pro to navigate this stuff.

In change in your premium, you may select to obtain a payout out of your annuity for the remainder of your life or a selected period of time. Sounds fairly good, proper? Properly, not so quick. That’s just about the place the great things ends.

We’ll get into all of the downsides later, however we’ll simply inform you proper now: Annuities aren’t value your time. The low fee of return gained’t even sustain with inflation. Keep away! You are able to do a lot higher with good growth stock mutual funds which have a ten–12% fee of return over time.

Variable Annuities

Variable annuities, however, are a bit completely different. They’re mainly mutual funds stuffed inside an annuity. So, in contrast to mounted annuities, your funds in retirement will depend upon how nicely the mutual funds you select carry out. That’s why they’re variable.

With a variable annuity, the account grows tax- deferred. Meaning you’ll should pay revenue taxes on no matter development the annuity makes once you begin taking cash out in retirement. We’ll speak extra about variable annuities in a minute.

What Are the Advantages of an Annuity?

With regards to a set annuity—there are not any advantages. Simply don’t. There’s by no means—ever—a case the place mounted annuities are the most suitable choice. Zilch. Zero. Huge goose egg!

Now, there are some advantages to having a variable annuity (although they do not outweigh the cons). For starters, you may select a beneficiary in your annuity so the funds you have been getting can go to a cherished one once you die.

Some variable annuities even supply a assure in your principal funding. So mainly, if you happen to put $200,000 into an annuity and the worth of the funding drops beneath that, you’ll nonetheless get your $200,000 once you take your cash out.

And in contrast to a 401(okay) or an IRA, annuities don’t have yearly contribution limits, so you may put as a lot cash into an annuity as you’d like.

Not so dangerous, proper? However pump the brakes for a minute. There’s a motive why many individuals who look into an annuity cease lifeless of their tracks and run the opposite manner earlier than signing on the dotted line.

What Are the Downsides of an Annuity?

Annuities are slowed down by quite a bit of charges that reduce into the return in your funding and hold your cash tied up. Yep—if you wish to get your fingers on the cash you’ve put into an annuity, it’ll price you. That’s a giant motive why we do not advocate annuities.

Keep in mind, annuities are mainly an insurance coverage product the place you switch the danger of outliving the cash you’ve saved for retirement over to an insurance coverage firm. And that comes at a steep value.

Annuities have manner too many charges.

If you wish to know, listed here are simply a few of the charges and prices you’ll see connected to an annuity:

- Give up prices: These can actually journey you up if you happen to’re not paying consideration. Most insurance coverage firms set a restrict on how a lot you may take out for the primary a number of years after you purchase an annuity, referred to as the give up cost interval. You’ll be charged a price on any cash you’re taking out past that restrict, and people prices can price you a reasonably penny. And that’s on high of the ten% tax penalty you must pay if you happen to take out your cash earlier than age 59 1/2!

- Commissions: One of many explanation why insurance coverage salesmen love pitching annuities to of us is that they get massive commissions from promoting annuities—even as much as 10%. Generally these commissions are charged individually, and different occasions these give up prices we simply talked about cowl the fee. While you’re listening to a gross sales pitch for an annuity, be sure to ask how a lot of a reduce they’re getting.

- Insurance coverage prices: These may present up as mortality and expense threat prices. Principally, these prices cowl the danger the insurance coverage firm takes on after they promote you an annuity, they usually’re normally 1.25% of your account stability per 12 months.5

- Funding administration charges: These are simply what they sound like. It prices cash to handle mutual funds, and these charges cowl these prices.

- Rider prices: Some annuities supply further options you may add to your annuity—issues like long-term care insurance coverage and future revenue ensures. These extras are referred to as riders, they usually’re not free—there’s a price for them too.

See what we imply? Take a look at all these charges! Insurance coverage firms make it virtually unimaginable to get to your cash with out paying an arm and leg. All these sneaky prices for a month-to-month verify? No. We’ll take our money up entrance after we retire, thanks very a lot.

Annuities most likely gained’t sustain with inflation.

Like we talked about earlier than, annuities (particularly a set annuity) almost definitely gained’t sustain with inflation. The speed of return is simply too low, and glued funds will lose their worth over time. Put it this manner: The typical price of a used automobile in 1990 was round $6,800.6 For 2022, used automobile costs hit a median of about $31,500.7 Let’s say you could have a set fee of $2,700 monthly. It doesn’t look nearly as good now, does it?

Annuities are very arduous to switch.

There’s a motive why insurance coverage firms use the wording give up interval. You’re primarily surrendering your cash to them! After which, if (or when) you discover a higher funding—like a Roth IRA or a Roth 401(okay)—you may’t even switch your cash out with out paying massive charges! You have got rather more management (and higher returns) with different retirement options.

Annuities are complicated.

For having a easy definition, annuities positive are complicated, aren’t they? Insurance coverage firms, salespeople and even your “savvy” brother-in-law will throw numerous buzzwords at you after they’re making an attempt to promote you an annuity, like risk-free, assured and secure. You may even hear fear-tactic questions like, “What if you happen to outlive your retirement financial savings?”

Look, something that needs to be bought to you this difficult most likely isn’t the very best thought—particularly if it makes your head spin. There are such a lot of particulars, further charges and extra options to think about. And albeit, they only aren’t definitely worth the hassle.

Right here’s the factor: Should you observe the 7 Baby Steps and make investments 15% of your revenue (Child Step 4) in your 401(okay) and Roth IRA (with good development inventory mutual fund choices), you’ll retire with a pleasant nest egg. A ten–12% fee of return will greater than sustain with inflation, and you’ll develop your cash with out paying insane charges. Easy, proper? We like easy.

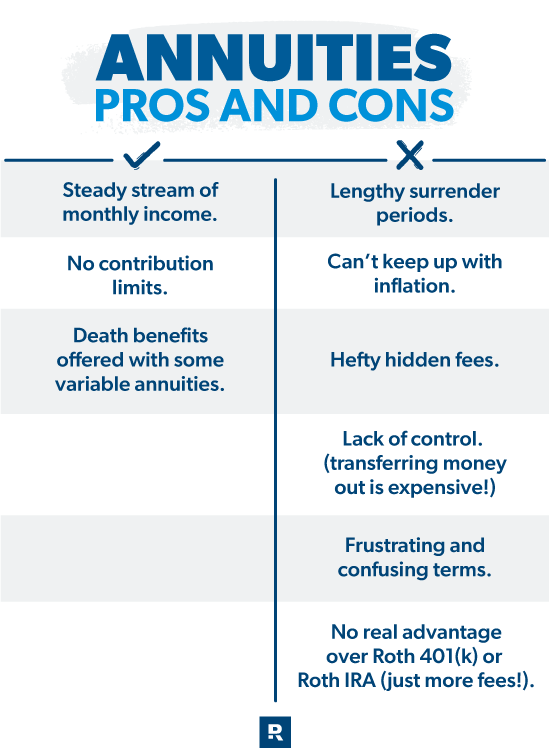

Execs:

- Regular stream of month-to-month revenue

- No contribution limits

- Dying advantages supplied with some variable annuities

Cons

- Prolonged give up durations

- Can’t sustain with inflation

- Hefty hidden charges

- Lack of management (transferring cash out is dear)

- Irritating and complicated phrases

- No actual benefit over Roth 401(okay) or Roth IRA (simply extra charges!)]

Instance of an Annuity

Meet Sally. Sally is 50 years previous and has had a great profession. She plans to retire at 60, and she maxes out her Roth 401(okay) and Roth IRA contributions yearly. She will get an inheritance of $10,000 (let’s hold the numbers easy) and decides to purchase a deferred variable annuity, utilizing her inheritance because the premium.

Now, as a result of Sally purchased a variable annuity, the insurance coverage firm invests her premium in mutual funds. Through the accumulation section, her cash will increase or decreases primarily based on the fund’s efficiency. Let’s say the fund averages a ten% fee of return—as soon as Sally retires, she ought to have simply over $27,000 in her annuity.

Sounds nice, proper? However take into accout: Sally can pay fee, insurance coverage prices, and funding administration charges on her cash—to not point out any further rider charges. Since Sally has already invested in different conventional accounts, this doesn’t damage as a lot. However her annuity payouts find yourself simply being sprinkles on the sundae of the retirement financial savings she constructed herself.

Are Annuities Ever a Good Concept?

We will come proper out and say it: For most individuals, an annuity simply doesn’t make sense. Whereas a assured revenue is nice, you could have far more earning potential with mutual funds by way of your 401(okay) or Roth IRA.. In actual fact, we discovered that the primary contributing issue to millionaires’ excessive internet value is investing in office retirement plans.8

Nonetheless, a variable annuity may make sense for some people who find themselves additional alongside of their investing. The one time it’s best to even take into consideration including a variable annuity to your funding technique is once you’ve already paid off your home fully and maxed out all of your different tax-favored retirement plans. Meaning you’re contributing as much as the restrict in your 401(okay) and Roth IRA.

Even then, there are a couple of different funding choices it’s best to look into earlier than annuities—like well being financial savings accounts, taxable funding accounts and even actual property. You possibly can sit down with an investing professional who can assist you type by way of the great, the dangerous and the (typically) ugly of every possibility. Keep in mind, by no means spend money on something you don’t perceive.

Annuities are not a substitute for conventional tax-advantaged retirement accounts. And by no means put a retirement account that already has tax benefits into an annuity. You don’t get any further tax advantages from placing your 401(okay) or IRA funds into an annuity—solely extra charges. Go!

Speak With an Investing Skilled

On the finish of the day, it’s as much as you to safe your monetary future, not an insurance coverage firm. In order for you the retirement of your goals, it is advisable to use an funding technique that works and stick with it. Should you’re able to get began, take a look at SmartVestor. It’s a free, simple option to get related with funding professionals in your space who know their stuff—they usually’re wanting to work with you!

{kind=link}